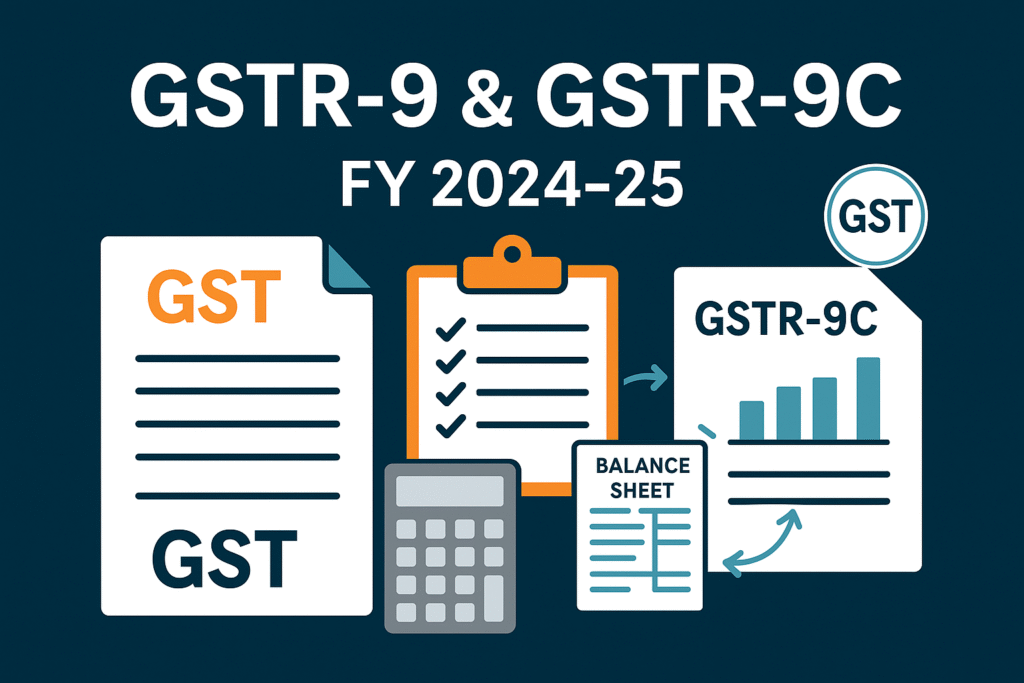

GSTR-9 is the annual GST return that registered taxpayers must file to consolidate their entire year’s transactions. This comprehensive return covers outward supplies, inward supplies, input tax credit, and tax payments for businesses with annual turnover exceeding Rs. 2 crores.

This guide is designed for GST-registered businesses, tax professionals, chartered accountants, and finance teams who need to understand and comply with GSTR-9 filing requirements for FY 2024-25.

We’ll walk through the fundamental requirements and eligibility criteria for GSTR-9 filing, including who must file and the current turnover thresholds. You’ll also learn about the critical compliance timeline and due dates, helping you avoid late fees and penalties. Finally, we’ll break down the step-by-step filing process and common challenges, so you can navigate potential pitfalls and ensure accurate submission.

Whether you’re filing GSTR-9 for the first time or looking to streamline your annual compliance process, this comprehensive guide covers everything from basic concepts to advanced filing strategies for the current financial year.

Understanding GSTR-9 Annual Return Fundamentals

What is GSTR-9 and its primary purpose

GSTR-9 is an annual GST return that must be filed by registered taxpayers to provide a comprehensive overview of their business transactions for an entire financial year. This consolidated return serves as a reconciliation mechanism that brings together all the monthly or quarterly returns (GSTR-1, GSTR-2A, GSTR-2B, and GSTR-3B) filed during the relevant financial year.

The primary purpose of GSTR-9 extends beyond simple data consolidation. It consists of detailed information regarding outward and inward supplies made or received during the financial year under different tax heads including CGST, SGST, IGST, along with cess and HSN codes. This return facilitates extensive reconciliation of data to ensure 100% transparent disclosures between what has been reported monthly and the actual annual figures.

For FY 2024-25 onwards, businesses with aggregate turnover exceeding Rs. 2 crores must mandatorily file GSTR-9, while it remains optional for those below this threshold. The due date for GSTR-9 filing is December 31st of the year following the particular financial year, making the GSTR-9 last date for FY 2024-25 as December 31, 2025.

Key components and consolidation requirements

The GSTR-9 form is systematically organized into 6 parts and 19 sections, each designed to capture specific aspects of business operations. The form requires annual sales data, carefully bifurcated between supplies that are subject to tax and those that are not subject to tax.

On the purchase side, businesses must disclose the annual value of inward supplies and the Input Tax Credit (ITC) availed on these transactions. These purchases require classification into three distinct categories: inputs, input services, and capital goods. Additionally, details of ITC that needs to be reversed due to ineligibility must be meticulously entered.

The consolidation process involves rigorous reconciliations that go beyond simple data compilation. Any short payment of tax or excess tax credit claims identified during this process must be settled with the government through proper channels. This comprehensive approach ensures that all discrepancies between monthly filings and actual annual figures are properly addressed and reconciled.

Different types of annual returns (GSTR-9, 9A, 9B, 9C)

The GST framework provides for four distinct types of annual returns under CGST Rule 80, each designed for specific categories of taxpayers:

GSTR-9 is designated for regular GST taxpayers who file GSTR-1 and GSTR-3B returns. This applies particularly to businesses that exceed the annual turnover threshold of Rs. 2 crores during the financial year.

GSTR-9A was originally intended for composition taxable persons and was required until FY 2018-19. However, from FY 2019-20 onwards, this requirement was replaced with the GSTR-4 annual return, which is due on April 30th of the following financial year.

GSTR-9B is specifically applicable to e-commerce operators who collect Tax Collected at Source (TCS) and file GSTR-8 monthly returns. However, the filing of this annual return is currently on hold.

GSTR-9C represents the Annual Reconciliation Statement, which functions as an audit form. This must be self-certified and filed by all taxpayers whose aggregate turnover exceeds Rs. 5 crores in a financial year, providing an additional layer of verification and compliance assurance.

Now that we have covered the fundamental aspects of GSTR-9 and its variants, it’s important to understand that certain categories of taxpayers are exempt from filing GSTR-9, including casual taxable persons, input service distributors, non-resident taxable persons, and those involved in TDS or TCS collections under specific GST provisions.

GSTR-9 Filing Requirements and Eligibility

Who must file GSTR-9 annual return

All GST registered taxpayers whose annual turnover exceeds Rs. 2 crores must file GSTR-9 annual return. This mandatory filing applies to regular taxpayers who file GSTR-1 and GSTR-3B returns during the financial year. The filing requirement operates at the GSTIN level rather than entity level, meaning businesses with multiple registrations under the same PAN must file separate GSTR-9 returns for each GSTIN.

Even if a taxpayer maintains regular taxpayer status for just a single day within the financial year, they become liable to file GSTR-9. This includes scenarios where businesses transition between different GST schemes during the year.

However, certain categories of taxpayers are exempted from GSTR-9 filing:

- Casual Taxable Persons

- Non-resident Taxable Persons

- Input Service Distributors

- Persons collecting Tax Collected at Source (TCS) under section 52 of CGST Act

- Persons paying Tax Deducted at Source (TDS) under section 51 of CGST Act

Turnover threshold limits and exemptions

The government has established a turnover threshold of Rs. 2 crores to determine GSTR-9 filing obligations. For businesses with aggregate turnover up to Rs. 2 crore, GSTR-9 filing has been made optional since FY 2017-18 onwards. This exemption was introduced to reduce compliance burden on smaller businesses.

The latest notification CGST notification 15/2025 confirms that registered persons with aggregate turnover up to Rs. 2 crore are exempt from filing annual returns for FY 2024-25 onwards. This exemption applies to the aggregate turnover across all registrations under a single PAN within the same state or union territory.

For taxpayers exceeding the Rs. 5 crore turnover threshold, additional compliance requirements apply through GSTR-9C reconciliation statement filing, which mandates audit and reconciliation between GSTR-9 data and audited financial statements.

Special cases for composition scheme taxpayers

Composition scheme taxpayers follow different annual return requirements. Instead of filing GSTR-9, they must file GSTR-9A (though this has been replaced with GSTR-4 annual return from FY 2019-20 onwards, due on 30th April of the following year).

When taxpayers transition between regular and composition schemes within the same financial year, they face dual filing obligations:

- GSTR-9 for the period when registered as regular taxpayer

- GSTR-9A/GSTR-4 for the period under composition scheme

This dual requirement ensures complete coverage of all transactions throughout the financial year, regardless of the GST scheme applicable during different periods.

Registration cancellation scenarios

Registration cancellation during the financial year does not exempt taxpayers from GSTR-9 filing obligations. If a business was registered under GST for any period during the financial year, even a single day, the annual return must be filed for the entire period of registration.

The filing covers all transactions from the beginning of the financial year up to the date of registration cancellation. This ensures complete disclosure of business activities during the period when GST registration was active, maintaining transparency in tax compliance even after business cessation or registration cancellation.

Critical Due Dates and Compliance Timeline

Annual filing due date of December 31st

The statutory due date for filing GSTR-9 for FY 2024-25 is December 31st, 2025. This represents a consistent pattern established by the GST authorities, where the annual return must be submitted by December 31st of the year following the relevant financial year. For instance, businesses completing their financial year ending March 31, 2025, must file their GSTR-9 by December 31, 2025.

It’s important to note that while December 31st remains the statutory deadline, the government has historically announced extensions closer to the actual due date. Taxpayers should monitor CBIC and GSTN updates regularly for any official extension notifications, as these extensions are typically announced through government circulars or notifications.

Pre-conditions before filing GSTR-9

Before attempting to file GSTR-9, taxpayers must ensure all prerequisite monthly and quarterly returns are completed. The GST portal automatically enables GSTR-9 filing functionality only after all due GSTR-1 and GSTR-3B returns for the entire financial year have been filed successfully.

The key pre-filing requirements include:

- Complete GSTR-1 filing: All monthly GSTR-1 returns for FY 2024-25 must be submitted

- Submit all GSTR-3B returns: Every monthly GSTR-3B for the financial year must be filed

- Perform comprehensive reconciliation: Conduct in-depth ITC reconciliation and sales reconciliation from the beginning of the financial year

- Vendor and customer communication: Address any gaps identified during reconciliation processes

- Tax payment settlements: Pay any short payment of tax or excess ITC claims through DRC-03 before filing

The auto-population feature in GSTR-9 depends entirely on data from previously filed returns, making complete monthly compliance essential for accurate annual return preparation.

Impact of delayed monthly return filings

Delayed monthly return filings create significant complications for GSTR-9 preparation and submission. When GSTR-1 or GSTR-3B returns remain pending for any month within FY 2024-25, the GSTR-9 filing functionality remains disabled on the GST portal.

This creates a cascading effect where:

- Portal restrictions: The system prevents GSTR-9 filing until all monthly returns are current

- Auto-population failures: Tables 4, 5, 6, 8, and 9 of GSTR-9 cannot be auto-populated without complete monthly data

- Reconciliation challenges: Incomplete monthly filings make year-end reconciliation extremely difficult

- Extended compliance timeline: Businesses must first clear all pending monthly returns before addressing annual compliance

Additionally, GSTN has implemented restrictions preventing taxpayers from filing GSTR-3B after three years from the due date, making timely monthly compliance even more critical for maintaining filing capabilities.

Extension possibilities and notifications

The GST authorities have consistently provided extensions for GSTR-9 filing deadlines in previous years, though these are announced closer to the statutory due dates. For FY 2024-25, taxpayers should anticipate potential extensions while preparing for the December 31st deadline.

Historical patterns show that extensions are typically announced through:

- CBIC notifications: Official government circulars modifying due dates

- GST Council recommendations: Policy decisions made during council meetings

- GSTN advisories: Technical updates regarding portal functionality and deadlines

The 55th GST Council meeting indicated that clarifications regarding late fee structures would be issued, suggesting ongoing policy refinements. However, businesses should not rely solely on potential extensions and must prepare for timely filing by the statutory deadline.

Recent notifications have also provided relief measures, such as the CGST notification 15/2025, which exempts registered persons with aggregate turnover up to Rs. 2 crore from filing annual returns for FY 2024-25 onwards, reducing compliance burden for smaller businesses while maintaining strict requirements for larger taxpayers.

GSTR-9 Form Structure and Content Requirements

Six parts and 19 sections breakdown

The GSTR-9 annual return is structured into six distinct parts containing 19 sections, each serving a specific purpose in comprehensive tax reporting. Part I covers basic details including GSTIN, legal name, and trade name of the taxpayer. Part II focuses on outward supplies, encompassing taxable supplies, zero-rated supplies, and exempt supplies. Part III details inward supplies subject to reverse charge, including goods and services from unregistered suppliers and imports.

Part IV addresses input tax credit (ITC) availability and utilization, while Part V covers payment of tax through cash ledger and other modes. Finally, Part VI includes refund claims and demands raised during the financial year. The 19 sections systematically capture turnover details, tax liabilities, and compliance information required for annual GST reconciliation.

Auto-populated data from GSTR-1 and GSTR-3B

The GST portal automatically populates significant portions of GSTR-9 using data from filed GSTR-1 and GSTR-3B returns throughout the financial year. Section 4 auto-fills outward supply details from GSTR-1 returns, including taxable supplies, zero-rated supplies, and exempt supplies. Similarly, Section 8 captures inward supply information from GSTR-3B filings.

Tax payment details in Section 9 automatically reflect amounts paid through GSTR-3B returns, including integrated tax, central tax, state tax, and cess payments. Input tax credit details from monthly GSTR-3B returns populate relevant ITC sections, ensuring consistency between periodic and annual filings. This auto-population mechanism reduces manual entry requirements while maintaining data integrity across GST returns for FY 2024-25 compliance.

Manual entry requirements for reconciliation

Despite auto-population features, taxpayers must manually enter several critical reconciliation items in GSTR-9. Section 5 requires manual input for amendments to outward supplies that weren’t reflected in the original GSTR-1 filings. Section 7 demands manual entry for supplies made to composition dealers and unregistered persons.

Reconciliation of annual audited turnover with GST turnover requires manual verification and adjustment entries. Any differences between books of accounts and GST records must be manually identified and reported. Interest and late fee payments, along with refund adjustments, require manual input to ensure accurate compliance reporting. These manual entries are essential for maintaining the integrity of annual GST compliance under the current filing framework.

HSN code reporting and negative amount entries

GSTR-9 mandates detailed HSN (Harmonized System of Nomenclature) code reporting for goods and SAC (Services Accounting Code) reporting for services. Taxpayers must provide HSN-wise summary of outward supplies in Section 12, including description, UQC, quantity, and taxable value. This requirement ensures proper classification and facilitates government revenue analysis.

Negative amount entries are permitted in specific scenarios, such as credit notes issued for supply reductions or input tax credit reversals. Section 4(B) allows negative entries for amendments reducing previously reported supplies. However, negative entries must be supported by valid business reasons and proper documentation. The system validates negative entries against prescribed limits to prevent misuse while accommodating legitimate business corrections in the annual return process.

Step-by-Step GSTR-9 Filing Process

Completing prerequisite monthly returns

Before initiating the GSTR-9 filing process, taxpayers must ensure all prerequisite monthly returns are filed and updated. The GST portal requires complete GSTR-1 and GSTR-3B data from the relevant financial year to auto-populate values in GSTR-9. Without these foundational returns, the annual return cannot be accurately prepared or filed.

The system generates GSTR-9 values based on data filed in GSTR-1, GSTR-3B, and auto-drafted information in GSTR-2A. Taxpayers can download comprehensive summaries including Form GSTR-1/IFF Summary (PDF), Form GSTR-3B Summary (PDF), and Form GSTR-9 System Computed Summary (PDF) to verify data accuracy before proceeding.

Performing comprehensive reconciliation exercises

With prerequisite returns completed, taxpayers must conduct thorough reconciliation exercises to identify discrepancies between books of accounts and filed returns. This critical step involves matching GSTR-2A data with input tax credit recorded in books, reconciling revenue general ledger with GSTR-1 sales data, and ensuring alignment between ITC claimed and purchase registers.

The reconciliation process extends to verifying HSN-wise summaries, validating tax computations across CGST, SGST, and IGST components, and identifying any reversed or ineligible ITC that requires adjustment. Any gaps discovered during reconciliation must be communicated to vendors and customers for resolution before final filing.

Online filing through GST portal

Now that reconciliation is complete, taxpayers can proceed with online filing through the official GST portal. The process begins by accessing www.gst.gov.in and navigating to Services > Returns > Annual Return or clicking the Annual Return link on the dashboard.

After selecting the relevant financial year and clicking the SEARCH button, taxpayers encounter a critical decision point – whether to file a NIL return or proceed with a detailed GSTR-9. NIL returns are applicable only when taxpayers have made no outward supplies, received no goods/services, claimed no credits or refunds, and have no other liabilities to report.

For non-NIL returns, the system displays the GSTR-9 Annual Return page where taxpayers can enter details across various categories including advances, inward and outward supplies, ITC availed, reversed ITC, tax payments, and HSN-wise summaries. The portal provides downloadable Excel templates and Table 8A document details to facilitate data entry.

Using offline tools and third-party software

Previously, taxpayers relied solely on manual data entry, but offline tools and third-party software now streamline the GSTR-9 filing process significantly. The government provides offline Excel-based tools that allow taxpayers to prepare returns offline and upload JSON files to the portal.

Third-party compliance software offers advanced features including automated data reconciliation, multi-GSTIN management at PAN level, GL-to-GST reconciliation capabilities, and built-in audit trails. These solutions provide auto-filling of GSTR-9 tables from GSTR-1, 2A, 3B data and books of accounts, along with comprehensive 17-point checklists that detect and flag potential mismatches before filing.

The software solutions also enable convenient downloading of multi-month GSTR-2A data, automated computation of outward HSN summaries from sales books for Table-17, and seamless JSON file generation for portal upload. With these tools, taxpayers can maintain consistent data sources across all GST compliances, reducing the risk of inconsistencies during annual return filing.

Late Fee Structure and Penalty Framework

Turnover-based late fee calculation

The GSTR-9 late fee structure is intricately linked to the taxpayer’s annual turnover, creating a proportional penalty system. For delayed filing of GSTR-9, regular taxpayers face a late fee of Rs. 200 per day (comprising CGST Rs. 100 and SGST Rs. 100), subject to specific maximum limits based on their turnover.

The maximum late fee is capped at either Rs. 5,000 or one-fourth (1/4th) of the taxpayer’s turnover in the respective state or union territory, whichever is lower. This turnover-based calculation ensures that smaller businesses aren’t disproportionately penalized while maintaining compliance pressure on larger entities.

For non-filing of GSTR-9, the penalty structure becomes more stringent. The maximum late fee extends to half (1/2) of the taxpayer’s turnover in the state or union territory, significantly increasing the financial impact for complete non-compliance compared to delayed filing.

Daily penalty rates and maximum limits

The daily penalty structure for GSTR-9 compliance operates on a consistent rate across different scenarios. Regular taxpayers incur Rs. 200 per day for both delayed and non-filing situations, with the distinction lying in the maximum limits applied.

For interstate supplies, the late fee remains at Rs. 200 per day, maintaining uniformity across transaction types. However, NIL GSTR-9 returns receive preferential treatment with a reduced daily penalty of Rs. 100 (CGST Rs. 50 and SGST Rs. 50), acknowledging the lower compliance burden for businesses with no taxable supplies.

| Filing Status | Daily Late Fee | Maximum Limit |

|---|---|---|

| Delayed Filing | Rs. 200/day | Rs. 5,000 or 1/4th of turnover |

| Non-Filing | Rs. 200/day | 1/2 of turnover in state/UT |

| NIL Returns | Rs. 100/day | Standard limits apply |

| Interstate Supplies | Rs. 200/day | As per turnover calculation |

Historical amnesty schemes and waivers

While the reference content doesn’t detail specific amnesty schemes, it’s evident that the government has implemented various compliance relief measures. The structured penalty framework itself suggests that authorities have considered the compliance burden on taxpayers, particularly evident in the differential treatment for NIL returns and the turnover-based maximum limits.

The penalty structure has evolved to balance compliance enforcement with practical business considerations, indicating that historical experiences have influenced current regulations. The fact that late fees are specifically structured with maximum limits based on turnover suggests lessons learned from previous compliance challenges.

Payment requirements before filing

Now that we understand the penalty structure, it’s crucial to note the payment methodology for these late fees. The late fees for GSTR-9 non-compliance must be paid in cash and cannot be adjusted against the input tax credit available in the taxpayer’s electronic credit ledger. This requirement ensures that penalties represent a real financial cost rather than a mere adjustment against existing credits.

Beyond late fees, taxpayers face additional financial obligations including interest charges. Delayed GST payment attracts interest at 18% per annum, while excess Input Tax Credit (ITC) claims result in 24% per annum interest. Reduced tax liability situations also incur 18% annual interest, compounding the overall compliance cost for non-adherent taxpayers.

The payment requirement extends beyond monetary penalties to include the underlying tax obligations. Taxpayers must clear all outstanding dues before being permitted to file their GSTR-9 annual return, creating a comprehensive compliance framework that ensures both procedural and substantive tax obligations are met.

Common Filing Challenges and Solutions

Reconciliation of GSTR-2A with Purchase Records

One of the most prevalent challenges in GSTR-9 filing involves reconciling GSTR-2A data with purchase records. This mismatch typically occurs due to data entry errors, timing mismatches, and vendor delays or omissions. The Input Tax Credit (ITC) claimed in GSTR-3B returns often doesn’t align with what’s reflected in auto-generated GSTR-2A/2B forms, creating significant compliance challenges.

The primary issue stems from invoices being excluded from GSTR-9 calculations based on place of supply criteria, where invoices specifying the supplier’s state instead of the recipient’s state are omitted. To address this challenge, businesses should ensure declarations are made promptly, especially for supplies related to a specific financial year. Regular cross-verification of claimed credits against GSTR-2A/2B is essential to avoid discrepancies that may result in notices from tax authorities.

Handling Additional Tax Liabilities

Managing additional tax liabilities during GSTR-9 filing presents complex scenarios that require careful attention. When mistakes in GSTR-1, GSTR-3B, or GSTR-4 cannot be corrected during the filing process, they result in incorrect reporting and potential additional tax obligations. This situation often leads to underreporting or penalties when businesses are unable to report specific sales or Input Tax Credit appropriately.

Businesses must maintain transparent reporting of Reverse Charge Mechanism (RCM) liabilities and ensure proper alignment of taxes filed under RCM with the claimed ITC for relevant supplies. The challenge becomes particularly acute during peak seasons when time constraints add pressure to the filing process, potentially leading to oversight of additional liabilities.

Managing ITC Reversals and Adjustments

Input Tax Credit reversals present multifaceted challenges in GSTR-9 compliance. Complex cases arise from non-payment to suppliers within the mandatory 180-day period, where businesses struggle with tracking vendor payments accurately. The failure to monitor these payments properly often results in unexpected ITC reversals that must be reflected in the annual return.

The process involves discovering accurate reversal provisions, computing precise reversal amounts, and correctly reporting these reversals in GSTR-9. Additionally, businesses face complications with ITC on exempt supplies, requiring precise computation while preventing input of restricted supplies. GSTR-9 also requires detailed bifurcation of all inputs, including input services and capital goods, which many businesses overlook, leading to challenges in gathering required information for accurate reporting.

Resolving Data Mismatches and Errors

Data compilation challenges become particularly pronounced when businesses attempt to consolidate financial data for entire fiscal years. High transaction volumes make it difficult to categorize transactions accurately into taxable, exempt, nil-rated, and zero-rated supplies, requiring thorough analysis and time-intensive processes.

Technical challenges compound these issues, with businesses experiencing difficulties on the GST portal, including problems copying negative values, non-reflection of DRC-03 payments, inability to upload JSON files, and challenges filing under DRC-03 despite available set-offs. The overlap in Tables 6(B) and 6(H) creates additional confusion, with overlapping figures concerning inward supplies and input tax credits requiring clearer understanding.

To mitigate these challenges, businesses should maintain complete records of all transactions, including invoices, payments, and tax-related documents. Implementing reliable GST software to automate calculations and generate reports significantly improves accuracy and streamlines the filing process. Regular consultation with tax consultants or Chartered Accountants provides essential guidance on complex issues, while staying updated on GST rules and regulations ensures compliance with evolving requirements.

Post-Filing Procedures and Limitations

ARN Generation and Confirmation Process

Once you complete the GSTR-9 filing process, the return status automatically changes to “Filed” on the GST portal. The system immediately generates an Acknowledgment Reference Number (ARN) as confirmation of successful submission. This ARN serves as your official receipt and proof that the annual return has been accepted by the tax authorities.

The GST portal sends automated notifications to confirm the filing – both SMS and email alerts are dispatched to your registered mobile number and email address. These notifications contain the ARN and filing confirmation details, ensuring you have immediate confirmation of successful submission.

After filing, you can access your submitted GSTR-9 return in multiple formats. The filed return becomes available for download in both PDF and Excel formats directly from the GST portal. You retain the ability to view, download, or print the return whenever required for your records or audit purposes.

Non-Revisable Nature of Filed Returns

A critical limitation of GSTR-9 filing is its permanent nature – once filed, no further changes or revisions can be made to the return. This non-revisable characteristic makes accuracy crucial during the preparation and filing process.

The system design prevents any modifications after submission, meaning any errors or omissions discovered post-filing cannot be corrected through amendments. This permanent nature emphasizes the importance of thorough review and reconciliation before final submission. Taxpayers must ensure complete accuracy in all details, calculations, and disclosures before clicking the final submit button.

Additional Payment Through DRC-03

Now that we have covered the filing limitations, it’s important to understand the mechanism for addressing post-filing tax liabilities. If any additional liabilities are identified after GSTR-9 filing, taxpayers can discharge these obligations through Form GST DRC-03.

This facility allows taxpayers to pay any short-paid tax amounts or settle excess input tax credit claims that may have been discovered during reconciliation activities performed after the annual return filing. The DRC-03 form serves as the designated channel for voluntary payment of additional tax liabilities without waiting for departmental notices.

Record Maintenance and Audit Trail Requirements

With the GSTR-9 filing complete, maintaining comprehensive records becomes essential for future compliance and audit requirements. The system provides an in-built audit trail at the invoice level for each entry, ensuring complete traceability of all transactions reported in the annual return.

Taxpayers must preserve all supporting documentation, reconciliation workings, and filing evidence for the prescribed statutory period. This includes maintaining copies of the filed return in both PDF and Excel formats, ARN confirmation, payment receipts for any DRC-03 payments, and complete reconciliation between books of accounts and GST returns.

The audit trail requirements extend beyond mere record keeping – businesses must ensure that all data sources used for GSTR-9 preparation remain accessible and verifiable. This comprehensive record maintenance supports potential departmental scrutiny and ensures compliance with GST audit requirements.

Filing GSTR-9 annual return is a critical compliance requirement for GST-registered taxpayers with turnover exceeding Rs. 2 crores. Understanding the form structure, meeting due dates, and ensuring accurate reconciliation of monthly returns are essential for seamless filing. The process requires careful attention to detail, from consolidating GSTR-1 and GSTR-3B data to addressing any discrepancies in input tax credit claims and tax payments.

The penalty structure for late filing varies based on turnover slabs, making timely compliance even more crucial. With the three-year limitation period for filing returns and the inability to revise GSTR-9 once submitted, businesses must prioritize accuracy and timeliness. Leveraging technology solutions and maintaining proper reconciliation throughout the year can significantly streamline the annual return filing process and ensure full compliance with GST regulations.