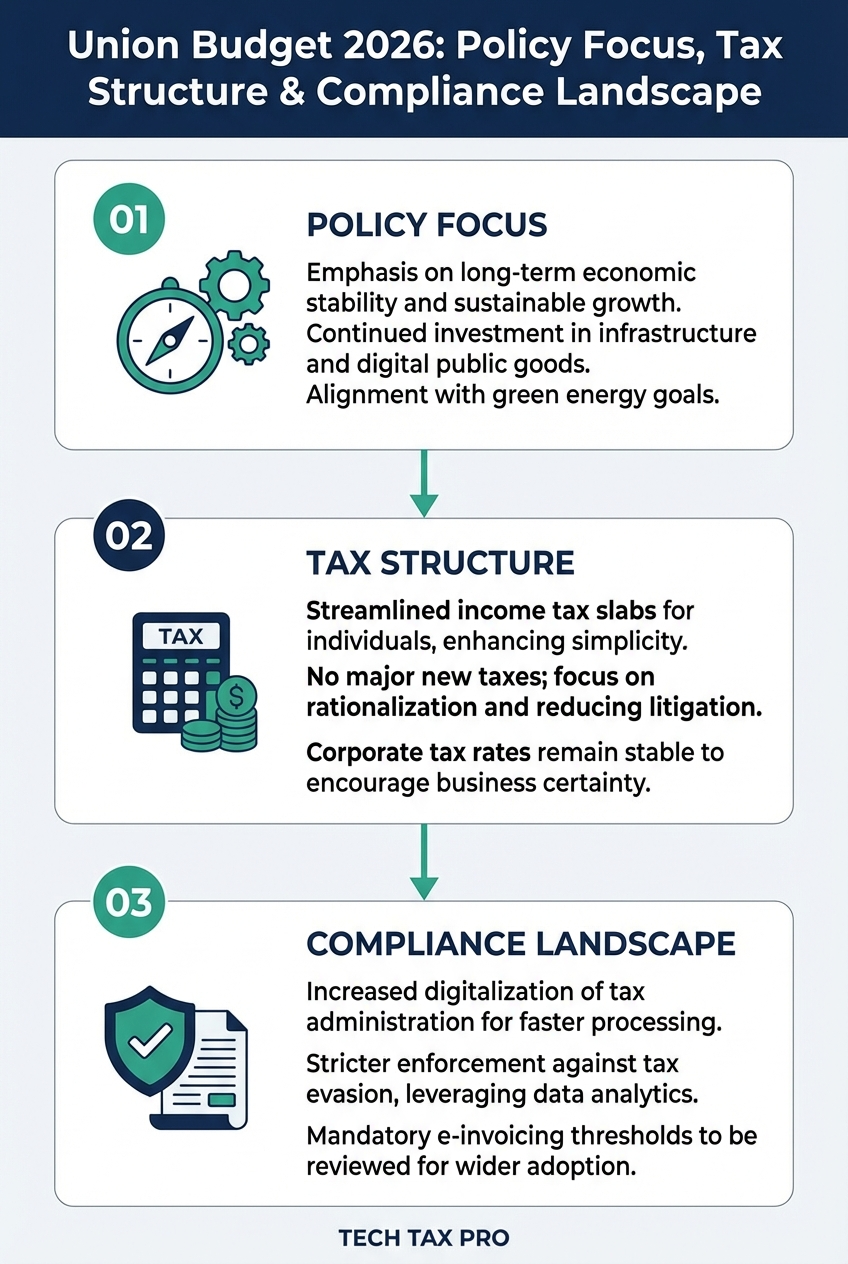

Union Budget 2026 Explained from a Chartered Accountant’s perspective focuses on what the Budget means for taxpayers, salaried individuals, and businesses, rather than headline-driven assumptions.

This year’s budget focuses on maintaining existing frameworks while making targeted adjustments. You won’t find dramatic overhauls in income tax provisions or major surprises in tax rates in Budget 2026.

We’ll walk through the key areas that matter most to your bottom line: how income tax rates and corporate tax structures remain largely unchanged, what this means for salaried class tax benefits and business incentives, and where the government is pushing digital tax compliance 2026 forward. You’ll also get insights into sector wise budget allocation 2026 and how these policy signals might shape your tax strategy going forward.

Whether you file individual returns or manage business finances, understanding these Union Budget 2026 changes helps you make smarter money decisions in the year ahead.

Income Tax Rates, Corporate Tax and Capital Gains: Status Quo Continues

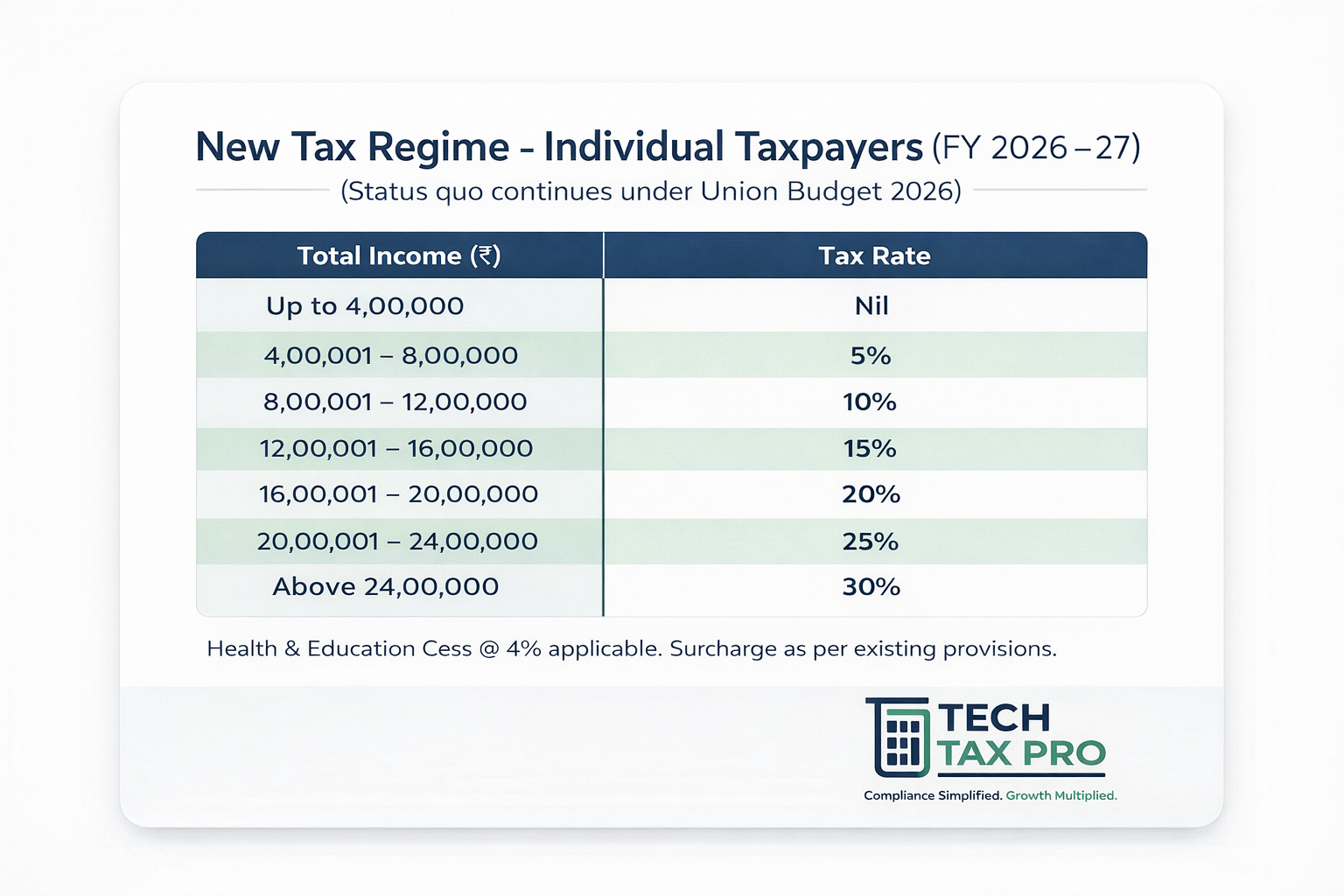

Income tax slabs for individual taxpayers

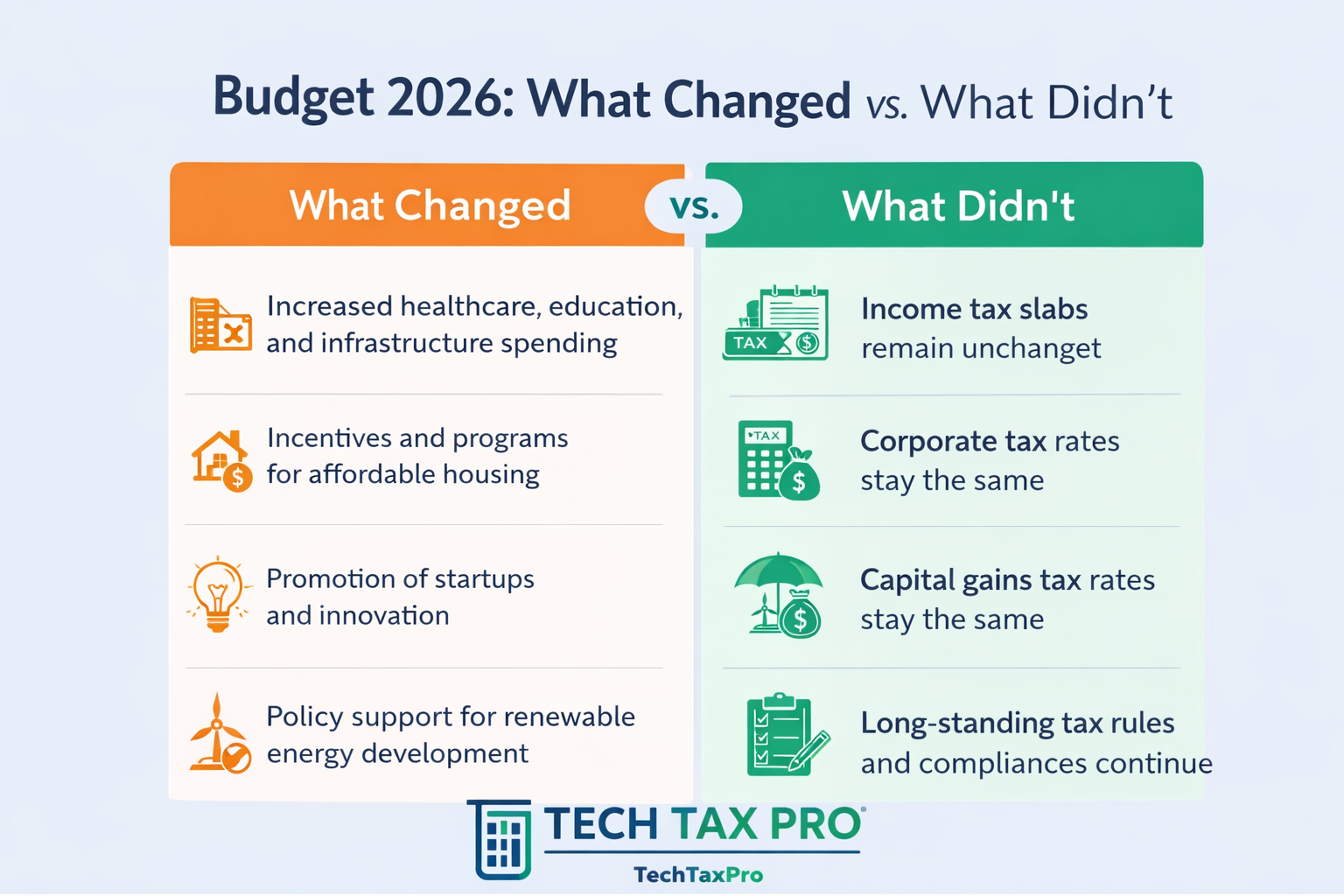

The Union Budget 2026 does not introduce any changes to income-tax slabs under either the old tax regime or the new default regime under section 115BAC. Taxpayers should continue to compute their tax liability based on the existing slab structure applicable for the year.

Corporate tax rate adjustments for different business sizes

Corporate tax rates remain unchanged in Budget 2026. Existing concessional regimes such as section 115BAA and section 115BAB continue subject to their prescribed conditions. No new turnover-based or sector-specific corporate tax rate reductions have been announced.

Capital gains tax modifications and their impact

Budget 2026 does not propose any changes to capital gains tax rates or exemption limits for equity, mutual funds, or real estate.

Surcharge and cess alterations affecting high earners

The surcharge structure and Health & Education Cess at 4% remain unchanged under Budget 2026.

Deductions and Exemptions for Individuals: No New Relief Announced

Standard Deduction Limits and Eligibility

No change has been announced in the standard deduction for salaried taxpayers or pensioners.

Deductions under Chapter VI-A

Existing deductions under sections such as 80C and 80D continue without any enhancement or expansion in Budget 2026.

Business Environment and Policy Support: Continuity with Targeted Signals

Startup and MSME policy direction

Budget 2026 continues the government’s focus on improving liquidity, ease of doing business, and regulatory certainty for startups and MSMEs, without introducing new tax exemptions or rate changes.

Manufacturing and industrial policy

The Budget reinforces the government’s long-term manufacturing strategy through policy support and customs-side measures rather than direct tax concessions.

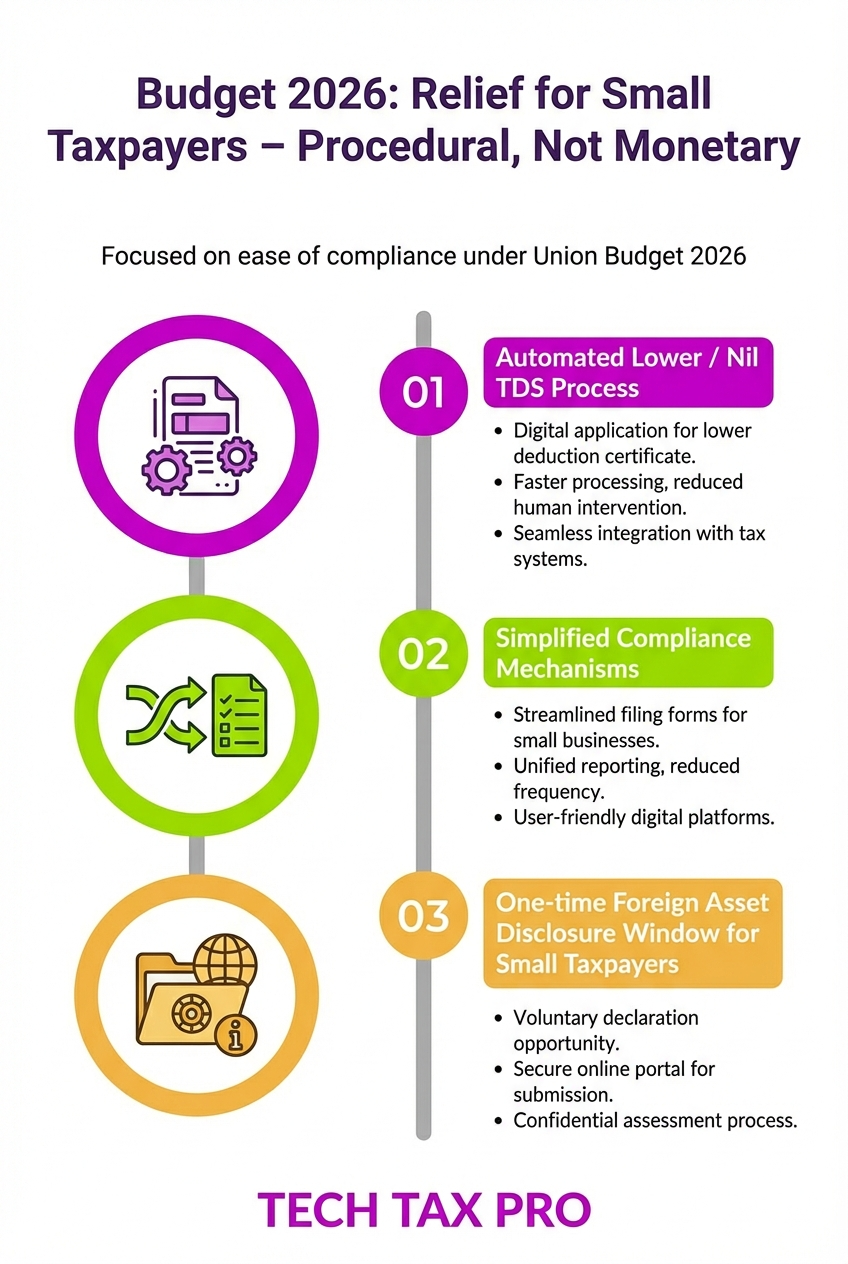

Relief measures for small taxpayers

Budget 2026 introduces procedural reliefs aimed at making tax compliance easier for small taxpayers. One key reform is the introduction of a rule-based automated process for obtaining lower or nil TDS deduction certificates, helping eligible individuals avoid unnecessary tax deduction at source without filing a manual application. Additionally, a one-time foreign asset disclosure scheme has been announced, offering eligible individuals a simplified window to disclose undisclosed foreign income or assets and avoid penalties or prosecution. These measures are focused on ease of compliance rather than reductions in tax rates or new tax rate slabs.

Compliance simplification and Digitalisation

Budget 2026 focuses on incremental improvements in digital systems and compliance processes rather than structural changes to GST rates or filing frameworks.

Sector-Wise Budget Focus and Its Financial Implications

Budget 2026 continues its emphasis on infrastructure, education, healthcare, and housing through sustained public spending, aimed at supporting long-term economic growth rather than immediate tax relief.

Union Budget 2026 adopts a measured and continuity-driven approach, focusing more on fiscal discipline, compliance stability, and long-term policy direction rather than sweeping tax relief measures. For individual taxpayers, salaried employees, and businesses, the Budget largely preserves the existing tax structure, with no major changes to tax slabs, deductions, or exemption limits. This signals the government’s preference for predictability and gradual reform over frequent structural changes.

The Budget’s emphasis on digitalisation, infrastructure-led growth, and sectoral support reflects a longer-term vision aimed at strengthening economic fundamentals rather than delivering immediate tax savings. While compliance processes are expected to become more efficient through technology and system improvements, taxpayers and businesses should plan on the basis of current law rather than anticipated relief.

From a practical standpoint, this is an appropriate time to review existing tax structures, regime choices, and compliance practices, rather than chase new deductions or incentives. Sound financial planning, accurate reporting, and timely compliance remain far more relevant than ever. As always, taxpayers and businesses should evaluate Budget implications in the context of their individual circumstances and seek professional advice where necessary, rather than relying on headline-driven interpretations.

Disclaimer

This article is intended solely for general informational and educational purposes. The analysis is based on the Union Budget 2026 speech and the Finance Bill as presented, along with provisions of the law as applicable at the time of writing. It does not constitute legal, tax, or professional advice, nor should it be relied upon as a substitute for personalised consultation.

Tax laws, interpretations, and procedural requirements are subject to change through subsequent notifications, circulars, judicial pronouncements, or amendments. Readers are advised to evaluate the Budget provisions in light of their specific facts and circumstances and to seek appropriate professional advice before taking any decision or action based on this information.